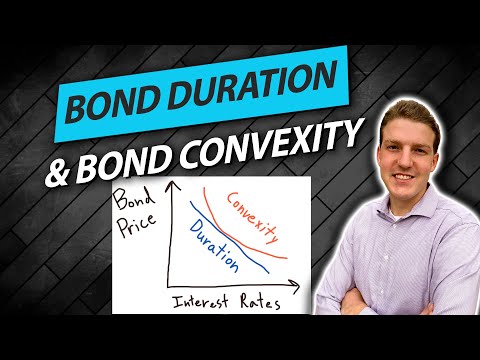

Bond Duration and Bond Convexity Explained

CFA Level I Fixed Income - Approximate Modified Duration and Convexity Adjustment

Convexity adjustment (for the @CFA Level 1 exam)

Bond Duration Explained Simply In 5 Minutes

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

CFA Level 3 | Fixed Income: Macaulay Duration, Dispersion and Convexity

Bond Convexity and Duration | Convexity explained with example | FIN-Ed

CFA Level I - Question Bank - Duration and Convexity Approach

Basics of Fixed Income Securities | Duration and Convexity | CFA Level I Fixed Income|MBA in Finance

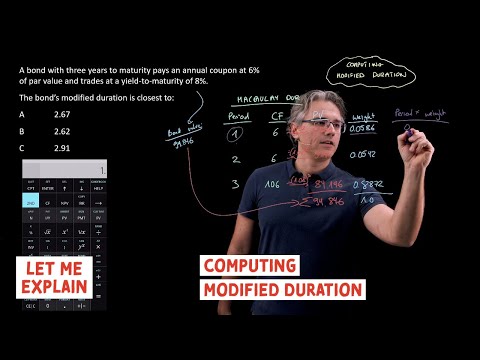

Computing modified duration (for the @CFA Level 1 exam)

Convexity of Bond

CFA Tutorial: Fixed Income (Bond Duration & Bond Convexity)

CFA® / FRM: Calculating Duration Convexity and its Effect on Bond Prices

Convexity

Duration 2 and Convexity

Complete illustration Duration , Modified Duration and Convexity

Deriving Duration and Convexity of a Bond

Convexity adjustment - CFA Level1 practice question

CFA level I: Fixed Income - Super Simplyfied Modified Duration Explained

Macaulay Duration