Convexity adjustment (for the @CFA Level 1 exam)

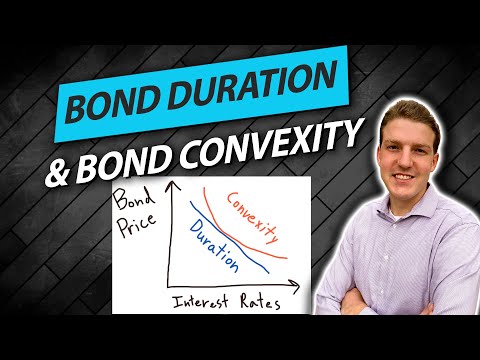

Bond Duration and Bond Convexity Explained

Option Adjusted Spread

OAS - Option adjusted spread (for the @CFA Level 1 exam)

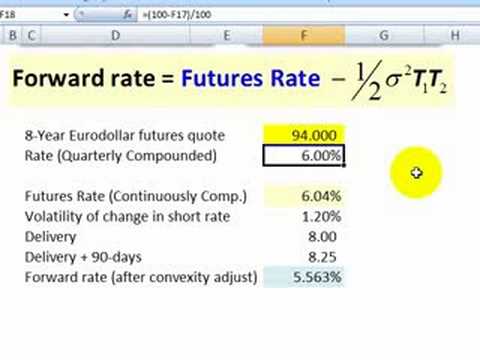

Convexity adjustment for Eurodollar futures

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

Convexity of Options and Arbitrage

Convexity of Options with Respect to Strike Price

Convexity Adjustment (Eurodollar Futures) (FRM Part 1, Book 3, Financial Markets and Products)

Convexity

Convexity adjustment - CFA Level1 practice question

Interest Rate Convexity

Fixed Income: Simple bond illustrating all three durations (effective, mod, Mac) (FRM T4-36)

Learn about Convexity

c explain why effective duration is the most appropriate measure of interest rate risk for bonds...

Fixed Income Derivatives - Options Adjusted Spread (OAS)

Z spread, Option adjusted spread, Spread duration & Convexity

Bond Convexity

Option-adjusted spread