IFRS 9 不良債権引当金の計算例と😇

Modelling For Provisioning Of Bad Debt Under IFRS 9 - Webinar Recording

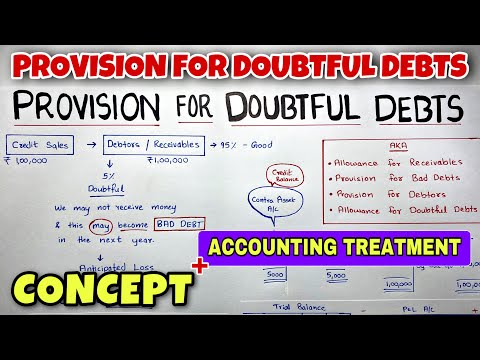

不良債権の会計処理

Allowance For Doubtful Accounts Explained with Examples

ECL Calculation Simplified / Practical Approach / IFRS 9

回収不能な債務および引当金 (不良債務および引当金) - パート 1

#1 疑わしい負債に対する備え - 不良債権 - サヘブアカデミー著

不良債権の会計処理 (仕訳) - 直接償却と引当金

Expected Credit Loss - IFRS 9/Ind AS 109 - The Concept

Allowance For Doubtful Accounts - Accounts Receivable

HOW TO AUDIT EXPECTED CREDIT LOSSES (ECL) IFRS 9: Accounts receivable valuation audit assertion

Lecture 1 - Expected Credit Loss (ECL) - CA Final IFRS 9 & Ind AS 109: Financial Instruments

Difference Between Bad Debts, Provision for Bad Debts, & RDD | Financial statements

First time adoption (IFRS 1) - ACCA SBR

PROVISION FOR CREDIT LOSS

Fact vs Myths in CA

Bad debts recovered journal entry

Expected Credit Losses model (ECL) IFRS 9 - نموذج خسائر الائتمان المتوقعة

Journal Entry for a Bad Debt Recovery

ECL Model | Credit Losses | Credit Risk | IFRS 9 | Financial Instruments | SBR | Dip IFRS |