二項式オプション価格モデル(CFA®およびFRM®試験のための計算)

BS Option Pricing Model Spreadsheet Tutorial

What is Binomial Option Pricing Model? | Binomial Pricing Model | Option Pricing Model(Hindi).

二項木(FRMパート1 2025 – ブック4 – 章14)

Binomial Model | Options | Concept Based Revision | CA Final SFM | CA Abhinav Sekhri | AIR 22 |

Option Pricing Binomial Model

二項モデルを用いたデリバティブの評価 - モジュール10 - デリバティブ - CFA® レベル I 2025 (および 2026)

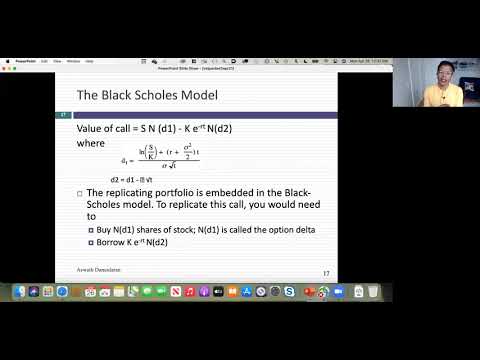

Session 9: Introduction to Option Valuation

Black-Scholes Option Pricing Model Spreadsheet

How to Price Options using a Binomial Tree (The Portfolio Approach)

Cython for Python speeding up Binomial Option Pricing model in Google Colab

Black Scholes Explained - A Mathematical Breakdown

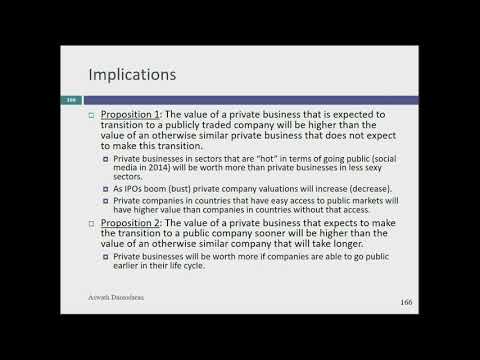

Session 21: Introduction to Real Options

Session 22: Real Options - Fact and Fiction

Session 22: Option Pricing Models and the Option to Delay

Derivatives - Options Valuation (Part 1) | Binomial & Risk Neutral Model | Portfolio Replication

Two Period Binomial Model ( American Call Option) l Ch. Derivatives l CA Final AFM

Session 22: Quiz 3 & First Steps on Options

Session 24: The Options to Delay & Expand

REAL OPTIONS GROWTH TIMING ABONDONEMENT OPTIONS DERIVATIVES FULL ENGLISH REVISION CA/CMA FINAL AFM