19. Black-Scholes Formula, Risk-neutral Valuation

Risk neutral probability measure simplified

Binomial Option Pricing: Tutorial on Risk Neutral Valuation

Binomial Option Pricing Model (Risk Neutral Valuation Approach) | FRM Part 1

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

Pricing Options Using the Binomial Tree (Risk Neutral Valuation Approach)

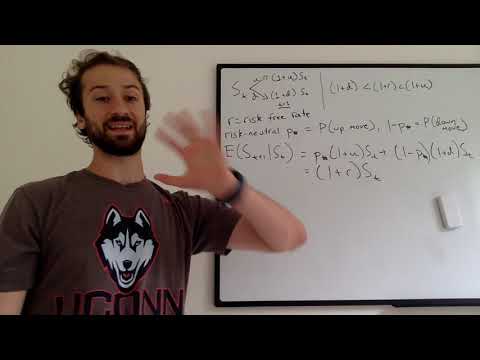

5. Risk Neutral Probability

FRM: Risk neutral valuation in option pricing model

Risk-neutral probabilities (FRM T5-07)

One Period Binomial Option Pricing: Risk Neutral Valuation

Simplified: Change of Probability Measure, and Risk Neutral Valuation

Pricing a Call Option using a Risk Neutral Tree Measure.

6 4 Risk neutral pricing Black Scholes Merton model Part 1

4 2 Risk neutral pricing Part 1

CFA L2- Risk Neutral Probability- Binomial Option Pricing Model

How I explain "Risk-neutral probabilities" to my Grandpa

CFA Level 1 | Derivatives: Deriving the Risk Neutral Probability

What is Risk Neutral?

Risk Neutral Valuation